DALLAS — Many banks choose not to make home loans to residents in low-income areas, government statistics show, even though federal law prevents discrimination in lending. But that doesn’t mean bank money isn’t flowing into these same neighborhoods. It is – but in the form of low-income apartment complexes built in areas of slum and blight.

A WFAA investigation found that banks own, or have owned, at least 50 low-income housing developments in Dallas. They buy into these projects in order to get billions of dollars in government tax credits on them and to prove to bank regulators that they are reinvesting in low-income communities.

Our investigation also found that regulators are failing to enforce laws that require these apartment complexes to provide a safe, affordable place for families to live, rather than merely be a tax boon for their owners.

A need for housing

Like most American cities, Dallas has a shortage of housing that lower-income families can afford.

When affordable housing does get built, it’s generally apartment complexes. And too often, developers construct them in high-crime, high-poverty neighborhoods located below Interstate 30.

Last year, we showed you how I-30 divides Dallas’ wealthier and whiter neighborhoods to the north from the largely Black and Hispanic residents to the south, and how many banks continue to “redline,” or purposely underserve, southern Dallas.

So, who’s the money behind all these low-income apartment complexes?

Sterlingshire

Let’s look at one – Sterlingshire, formerly called the Bruton Road Apartments. It’s at Bruton Road and North St. Augustine Drive in the heart of Dallas’ Pleasant Grove neighborhood.

From the outside, they’re nice. Residents we talked to said they’re also nice on the inside.

But crime is high, according to residents. The complex is inside one of the Dallas Police Department’s “Targeted Area Action Grids.” These TAAG areas, as they’re known, get extra police attention because of high crime, and are scattered mostly in southern Dallas.

Sterlingshire “should never have been [built] there to begin with,” said Terrance Perkins, a community activist and pastor of the nearby Abundance Grace Church.

“We need affordable housing,” he said. “But apartment complexes [are] something we need less of, especially here in Southeast Dallas. When you take a population of people and put them in one place, and no resources, you lead them to a dead end.”

So, who owns Sterlingshire? WFAA research of court filings, state housing records and public corporate documents shows that Bank of America owns 99.9% of the corporate entity that owns the complex.

And it’s not alone.

Too much crime, too many apartments

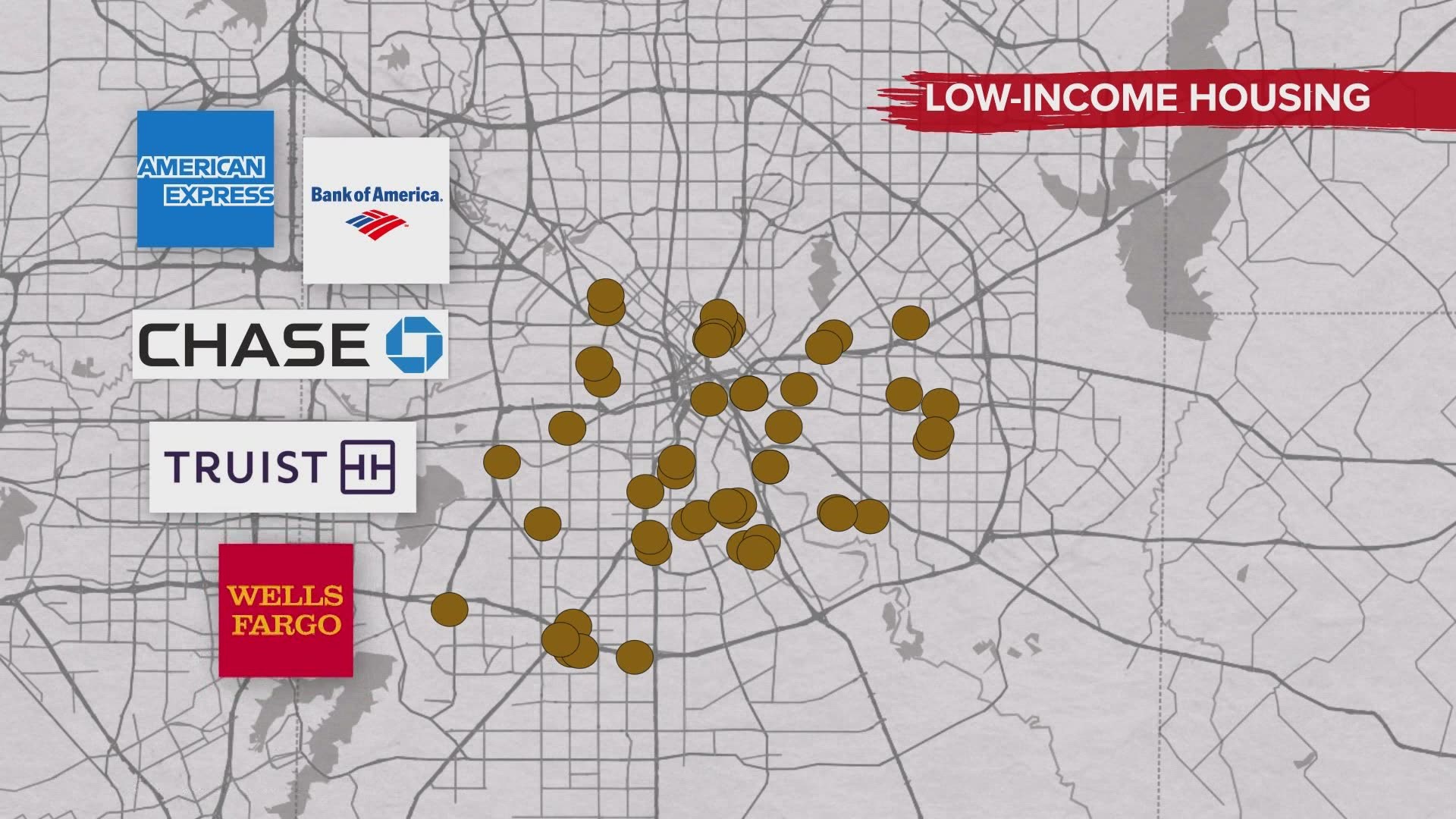

We’ve identified 50 affordable-housing apartment complexes in Dallas that are owned, or have been owned, by big national banks. In addition to Bank of America, these include American Express, Chase, Truist and Wells Fargo

We reached out to all of them. Those that responded said they are proud to invest in housing that serves low-income and minority families. But none wanted to be interviewed about it.

A roof over your head is, indeed, a good thing, housing advocates say. But if you look closer, frequently, these buildings are clustered together in the poorest parts of the city. They are in deserts with few jobs, under-performing schools, lacking retail, fresh groceries, or reliable transportation.

Half of the bank-financed apartments we’re talking about are located inside DPD’s TAAG areas, or crime hotspots.

State law says a neighborhood shouldn’t have more than 20% of its housing – apartment units or single-family homes – be government-subsidized rental properties. In other words, no clusters of low-income housing.

But we found several groupings of low-income housing complexes. One is near Southwest Center Mall, formerly known as Red Bird Mall, where we found banks own or have owned three apartment buildings. The concentration of subsidized housing there is 63%.

Farther east near C.F. Hawn Freeway and Great Trinity Forest Way is another high-crime, high-poverty, low-opportunity neighborhood. There you will find three apartment complexes, including Rosemont at Pemberton Hill, which was formerly owned by Chase Bank. The concentration of subsidized housing there is 43%.

In a statement, Chase Bank said: “We believe affordable housing is a critical need in our communities.”

“Where you live really matters,” said Ann Lott, a fair housing advocate at the Inclusive Communities Project in Dallas.

Her nonprofit has sued suburban communities over their refusal to allow affordable housing. Those refusals are one reason housing is continually built in the same inner-city neighborhoods. “We have to stop a system that consistently puts poor people in areas where they cannot thrive," she said.

“The people that live in the community need access to credit," she said. "They need access to loans so they can buy their homes. Banks are contributing to the slum and blight of the communities and one could argue that they have become the new slumlord.”

Bank report cards

So, why do national banks invest hundreds of millions of dollars in apartments in high-crime, high-poverty neighborhoods? That’s a two-part answer.

The first part has to do with bank exams.

First, a little history.

For decades, through a practice called redlining, banks denied loans to the Black and Hispanic communities.

To address the problem, Congress passed The Community Reinvestment Act in 1977, also known as the CRA. Every few years, the government grades banks on how well they follow the CRA; in other words, how good a job they are doing loaning money directly to lower-income businesses and homebuyers.

By the ’80s and ’90s, though, regulators changed the rules so banks don’t just get credit for making loans directly to individuals. They also give them what you might call "extra credit" for investments in affordable housing.

Today, the CRA “motivates the vast majority of these investments,” according to the Affordable Housing Tax Credit Coalition trade group.

Consider the CRA exam for Bank of America for its operations in North Texas. It says “...the bank has an excellent level of community development investments” totaling $813.9 million around Dallas-Fort Worth. That includes a $15.5 million dollar investment in Sterlingshire.

Corporate records show Bank of America is a 99.9% "silent partner" in Sterlingshire. That means the bank is a majority corporate owner but doesn’t make decisions about where an apartment complex is built, and it doesn’t run day-to-day operations.

In addition to Sterlingshire, Bank of America is also the 99.9% corporate owner of a low-income apartment complex across the street, and another two miles to the north.

In all, we found Bank of America has current or past investments in 13 low-income complexes in Dallas. All generate positive CRA scores for the bank.

Using public records, we estimate Bank of America has invested $50 million in the area around Sterlingshire alone.

But how much money is the bank lending to homebuyers in this same neighborhood? The government tracks that, and analysis provided by the advocacy group the National Community Reinvestment Coalition, or NCRC, shows Bank of America made two mortgage loans in that area in 2019.

We reached out to Bank of America about our findings.

"There is a tremendous need for affordable housing nationwide," said Bill Halldin, Bank of America spokesperson, in a written statement.

"Bank of America is committed to supporting our clients and communities by providing upfront financing that is a critical component for organizations to be able to expand housing opportunities," Halldin said.

Bank of America is not alone in its lending patterns.

Further analysis of government lending data by the NCRC shows that banks make a lot of loans north of I-30. To the south, banks make very few loans – but have invested hundreds of millions of dollars in affordable housing apartment complexes, helping them get passing grades on their CRA exams.

What does all this say about the effectiveness of the CRA?

“To allow tax credit housing to substitute for real loans, home loans -- it’s perverted the entire meaning of the Community Reinvestment Act," said Laura Beshara, a Dallas civil rights lawyer. She along with law partner Michael Daniel have filed a number of lawsuits over affordable housing policy, including for the Inclusive Communities Project, whose case went all the way to the Supreme Court.

"It’s furthered the racial concentration of the area, its furthered the poverty concentration," she said. "It’s added more residents to an area of high crime that didn’t need to be there. And, at the same time, they’re not making any loans to the people that live there.”

Tax credits

Aside from favorable CRA bank exam ratings, another reason banks buy into low-income apartment complexes is tax credits.

The government says, "Hey, Bank, if you buy in with $15 million to cover the cost of building XYZ apartments, the United States promises to pay you back." The bank then claims the tax credit over a 10-year period until it gets all its money back.

We're not talking about hundreds or thousands of dollars of these low-income housing tax credits. Each year, the United States gives about $8 billion in tax breaks to the corporate owners of these apartment complexes. And almost all of those tax breaks go to banks.

For the banks, “it’s a no-fail system,” Beshara said. With government support, she said these apartment investments generate a steady return for banks with almost no risk.

“It’s very safe from an investment point of view, and a sure thing,” she said,

But there are rules. To get that tax credit the government says a project has to be part of a “concerted community revitalization plan.” What does that mean?

It means to be eligible for a tax credit, apartments have to be located in parts of town where there is a focused plan to improve struggling neighborhoods. Typically, that means they have to be accompanied by things like health clinics, community centers, infrastructure, educational and economic opportunities.

Dallas has designated revitalization plans in five neighborhoods. All of them are south of I-30 and one is in West Dallas. Banks have financed a total of six affordable housing projects inside those zones. All of them get tax breaks.

But we found 44 apartment complexes in Dallas that were all built outside revitalization areas. And they got tax breaks, too.

“I don’t think they should be eligible for the tax credit,” Beshara said.

So, who’s letting this happen? First off, it is developers who conceive of the projects, pick the location, and get all the state and local approvals. Developers get fees from the projects and other revenue. Banks then buy into the projects as “limited partners,” and usually become 99.9% corporate owners.

By law, banks typically cannot own property, so they have to get special permission from the government to do so. That permission is granted by the Office of the Comptroller of the Currency, or OCC. They regulate banks, among other things, and give them permission to own a controlling interest in these apartment complexes. They also grade big national banks on how well they comply with the CRA.

We asked the OCC about its own rules that allow banks to buy into these low-income housing tax credit projects, or LIHTCs, only if they are “designed primarily to promote public welfare," and whether what we found is of concern to them.

"The OCC’s CRA rule does not require a (low-income housing tax credit) project to be in a revitalization area to receive CRA credit," said Bryan Hubbard, an OCC spokesman. "The OCC doesn’t regulate all individuals nor entities that may invest in LIHTC projects, and isn’t involved in selecting which projects receive LIHTCs."

Banks we contacted bristled at being called “owner” of these apartment complexes. They point out that they do not select the sites where they’re built, and do not run any of the day-to-day operations. All of which is true.

But federal law says they have to be an owner in order to use the tax credits to lower their tax bill.

“Under federal income tax law, (low-income housing tax credits) may be claimed only by property owners who have the benefits and burdens of ownership,” according to a 2014 OCC information sheet outlining how the program works. “This includes all partnerships (LPs, LLCs, and other equity investors) in the properties. For example, if a bank holds a 99.99 percent interest in a partnership, it receives 99.99 percent of the tax credits and real estate losses, which include, but are not limited to, depreciation and interest expenses.”

The tax credits themselves are granted by the Internal Revenue Service. But government investigations have found that the IRS does a poor job of overseeing the program.

In 2015, the U.S. General Accounting Office found “IRS oversight... has been minimal” and records “were not sufficiently reliable to determine if basic requirements for the LIHTC program were being achieved.”

“They don’t care where these projects go – at all,” Beshara said. “And they don’t care who it affects.”

We asked the IRS why it gives banks tax breaks on apartments that are outside revitalization areas. “Since your story involves a specific group of taxpayers in a certain area, the IRS will decline any comment due to disclosure laws and regulations,” a spokesperson replied in an email.

“The program has operated for over 30 years without any requirements of where the housing should be located,” Beshara said. “As a result, the housing has become concentrated in high minority areas of high poverty. Many of them with very distressed neighborhood conditions with high crime.”

Sterlingshire revisited

In 2015, before Sterlingshire was built, Beshara and her law partner sent a warning letter to regulators. They said Sterlingshire’s paperwork “failed to disclose” that there was “significant criminal activity” in the area and that the project should not be eligible for tax breaks.

“This false representation can be the subject of a suit by any future tenants of the project for the consequences, including harm from the high crime in the area,” they wrote.

That harm came in 2019. In June, 13-year-old Malik Tyler, a resident of Sterlingshire, was walking near his home when he was shot and killed in a drive-by shooting.

The company that manages Sterlingshire declined to talk to us for this story.

Not far from where Malik was killed, across the street from Sterlingshire, neighbors later noticed activity on a large, vacant lot. When Terrance Perkins inquired, he learned what developers had planned for the site – another low-income housing complex.

He gathered neighbors for a fight. They won that battle – at least for now. But another neighborhood might not be so lucky.

“What the builders end up doing, or the investors, they’ll come to a community that’s not going to fight it and put the apartment complex there,” Perkins said. “And then [they’ll] say, ‘Hey look, we’ve done something great.’ But in reality, you’re only crippling us.”

Got a story tip? Email dschechter@wfaa.com.