TEXAS, USA — It has been horrible to watch: A week ago WFAA was live as flames raced across a parched field of grass, jumped the fences and burned down a whole line of homes in a North Texas neighborhood.

In another location, a fire that started inside a home spread to the outside, where drought conditions whipped it into a wildfire that incinerated several more homes.

When you think of wildfires, California immediately comes to mind. Statistics show that last year that state led the nation with 9,260 wildfires. But Texas was second with 5,576.

Many of us may not realize it, but our properties could be vulnerable. Even before this unusually hot, dry summer, an analytics firm last year found that 717,800 properties in Texas are at high to extreme risk from wildfire.

Again, with that stat, Texas is second in the country only to California (which had 2,040,600 properties considered at high to extreme risk from wildfire).

You may be underinsured. Many homeowners are

Fire is one of many perils Texans face, which is why wfaa.com has published multiple reports in the past few years reminding homeowners to make sure they are not underinsured. See those reports here, here, and here. Each has good information for homeowners.

Beyond the usual perils, here’s the other reason to make sure you are not underinsured: Inflation.

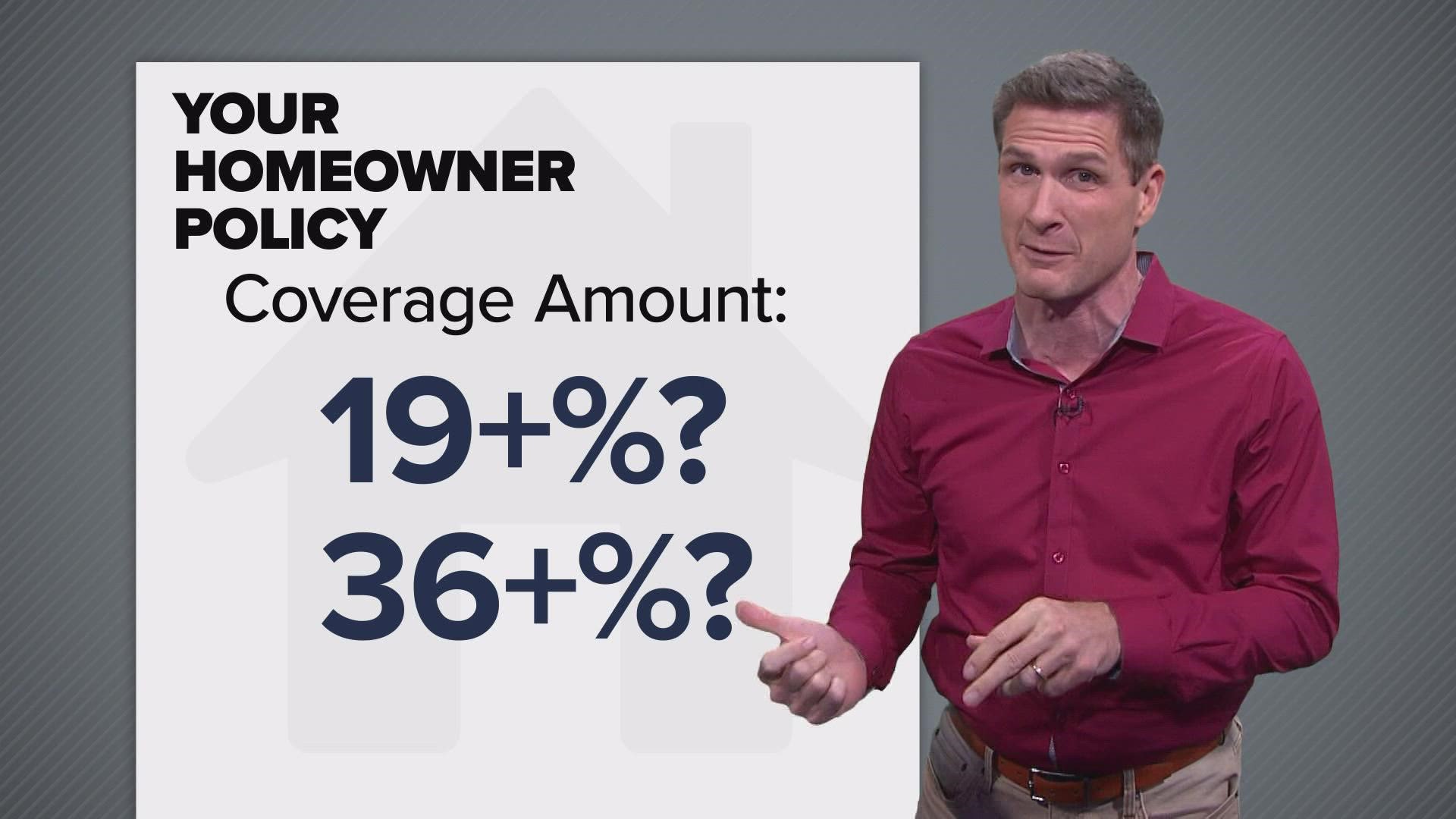

According to the National Association of Homebuilders, the costs of building materials have inflated 19.2% from a year ago, and 35.6% since the start of the pandemic. And add a big plus sign to that, because construction labor has also become a lot more expensive.

But has your homeowners insurance coverage increased by over 19% from a year ago? Or 36% or more since the start of the pandemic?

You may need to increase your coverage amount if you haven’t in a while. And your insurer doesn’t necessarily call you to do this. You should call them and run the numbers, especially if it has been a while. And shop around with others while you are at it.

The process is not fun… and increasing your coverage amount might cause your premium to go up. But protect your home; it’s likely your biggest investment.

Going back to the scenes of homes consumed by wildfires recently, the sight is awful enough. You don’t want to find out afterward that the check you will get isn’t enough to fully rebuild your dwelling.

It was estimated after the 2021 winter storm in Texas that 11% of homeowners in metro areas in Texas don’t have any insurance coverage on their dwellings. Almost 27% of people who live outside metro areas in Texas don’t have coverage. That’s a huge risk.

Even if you have coverage, statistics show that about two-thirds of us are underinsured. You can build in an automatic cushion by getting what’s called extended replacement coverage. That’ll take the amount you’re covered in your policy and extend it by anywhere between 10% and 50% extra. Estimates say that usually costs you $25-$50 more in your annual premium.

A more expensive guaranteed replacement cost will cover you no matter what it takes to rebuild. Estimates say that’ll usually cost you 5-10% of your total policy premium. Forbes published an article last year that detailed which carriers offer those additional coverages.

Whatever you do, just review your coverage, especially if you haven’t in a while.