TEXAS, USA — You know how home ownership comes with a whole list of chores? There’s one that homeowners might be tempted to put off; but doing so can cost you big.

Check your homeowner’s insurance!

A lot of people find out the hard way that they are underinsured. Nationwide Insurance says two thirds of homeowners don’t have adequate coverage; and that the average amount they are short on coverage is 22%.

So, what if you need $300,000 to rebuild, and you only get a check for 234,000?

Building costs are soaring

A big part of the problem is the surging cost of building materials, many items rising at a record pace.

According to the National Association of Home Builders, the overall cost of building materials is up 28.7% since January 2020. Lumber has been through some wild up and down swings, but the NAHB says lumber is up 73.9% just since September.

They add that in the past year, the price of steel has doubled, concrete is up 9.1%, drywall is 23% more expensive, and paint is up significantly (30.3% for exterior and 21.2% for interior).

And construction labor isn’t cheap either.

Builders say you can usually tell how much laborers are making by looking at the trucks out at job sites. They say they’ve been seeing some nice new trucks.

Do you have enough insurance coverage to keep up with the cost of rebuilding?

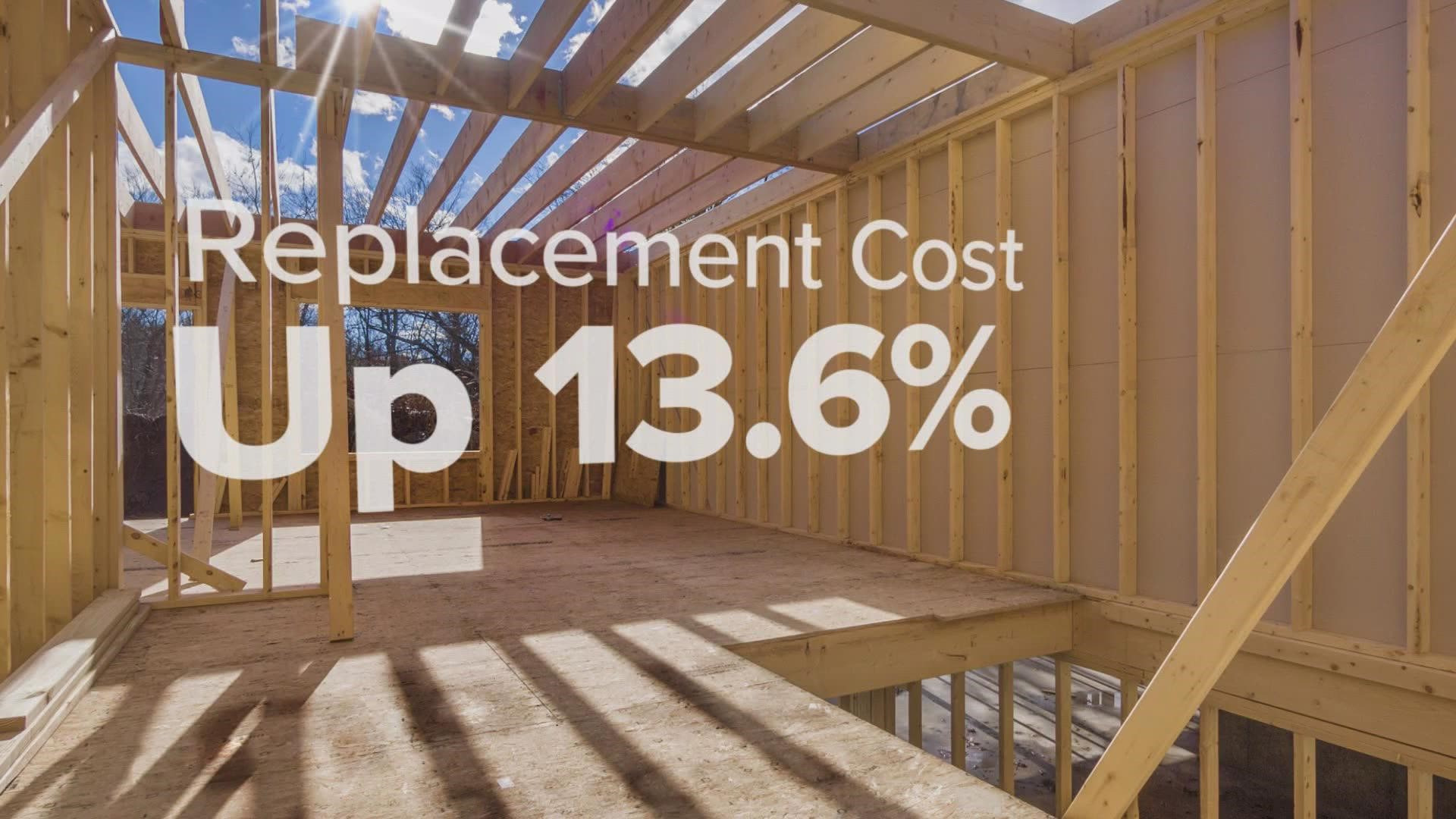

The Insurance Information Institute just announced that the cost to replace your home has gone up by 13.6%. Considering all of that, if something happens to your house and you have to rebuild, do you have enough insurance?

Maybe you have extended replacement cost coverage to make up for any potential shortfall. If not, look at when you last updated your homeowner’s policy. Even if it was last year, those dollar amounts may now be seriously outdated, and you may be woefully underinsured.

The institute has advice on how to avoid being underinsured.

Call your agent to talk about how much coverage you need and shop around to see if you are getting the best rate for that coverage. The process can be a hassle. But finding out the hard way that you don’t have enough is a lot worse than just getting to that dreaded item on the homeowner chore list.