DALLAS — It is time now for the fourth item on my list of things that I decided we needed to talk more about as I was studying to get my Texas real estate license.

This installment is about your "up payment." I actually did pass my real estate courses, so I know it's really called a down payment.

But the amount needed for a traditional 20% down payment is up quite a lot, so it seems fitting to change the name.

With the $249,900 median home price in Texas in April of 2020, you needed $49,980 for a 20% down payment. Three years later, in April of 2023, the median home price in Texas was $338,142, so you needed $67,628.40 to meet that 20% down payment threshold.

For some homebuyers, that kind of upfront payment is PMI -- pretty much impossible.

To remedy that, many of them must turn to a different PMI -- private mortgage insurance.

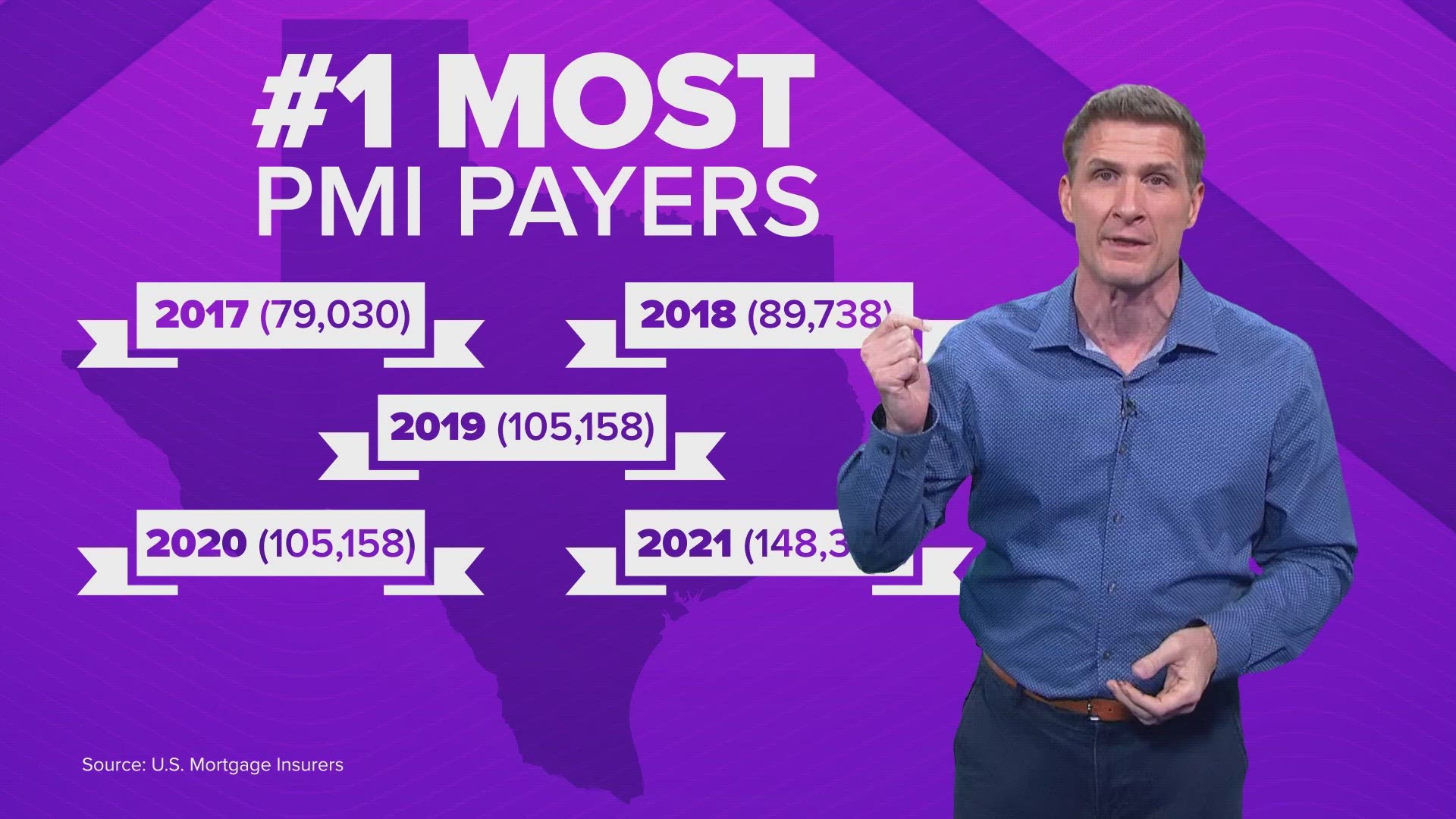

Texas keeps leading the country in the number of PMI payers

Over the summer, U.S. Mortgage Insurers released their latest report. It show that once again in 2022, Texas led the country in the number of homebuyers needing PMI programs to be able to get a conventional home loan. They report that 99,925 Texans in 2022 paid PMI. The report found that for six years in a row now, Texas has led the country in the number of homebuyers who opted to pay the extra monthly fee in return for a lower down payment to get a home loan.

Texas had the most homebuyers paying PMI in 2017 (79,030), 2018 (89,738), 2019 (105,158), 2020 (105,158), and 2021 (148,366).

PMI is an additional charge on top of your monthly house payment. It usually costs between $30 and $70 per month for each $100,000 you've borrowed.

So, if you borrowed $300,000, you'd pay between $90 and $210 extra each month for mortgage insurance. That's a wide range.

If you have to go the PMI route, shop around. The fee can vary from one lender to another.

My real estate courses explained that, historically, loans where the borrower made a 3% down payment have been foreclosed upon four times more often than loans with a 10% down payment.

That's why lenders want you to have this insurance, which protects them if you default.

How to stop paying PMI

Usually, you can request to stop paying PMI when you get down to where you just owe 80% of the home's "original" value.

So, if you bought a home for $500,000 with a down payment of less than 20%, you keep paying your mortgage until you get the loan balance down to $400,000, when you hit that magic mark -- 80% of the “original" value.

I keep saying original. But if your home's "current" value has appreciated well beyond the original value when you bought it (and many homes have), that alone could get you over the hump.

Remember our example: You hit the magic 80% when you get your loan balance down to $400,000 from the original $500,000 cost.

What if the home you bought for $500,000 has increased in value to $575,000?

In that scenario, your loan to current value ratio would reach 80% much sooner, when your loan balance hits $460,000.