DALLAS — Many Texans shopping for what they consider to be affordable automobile insurance have been finding that to be a dead-end street.

S&P Global Market Intelligence tracks this better than anyone, and they’ve highlighted that, between 2018 and 2023, auto insurance rates in Texas went up 46.5% -- the most in the country.

Why? There are many factors. A big part of the problem is the way we drive. If you are out on Texas roads, you have seen the problem. Maybe you’ve even been the problem.

Using the latest year for which we have complete data (2021), we can see that California had 27,113,000 licensed drivers compared to 18,298,000 in Texas. California also had far more registered vehicles (31,349,000) compared to Texas (23,013,000). And collectively, Californians traveled a lot more vehicle miles (311 billion) than Texans (285 billion).

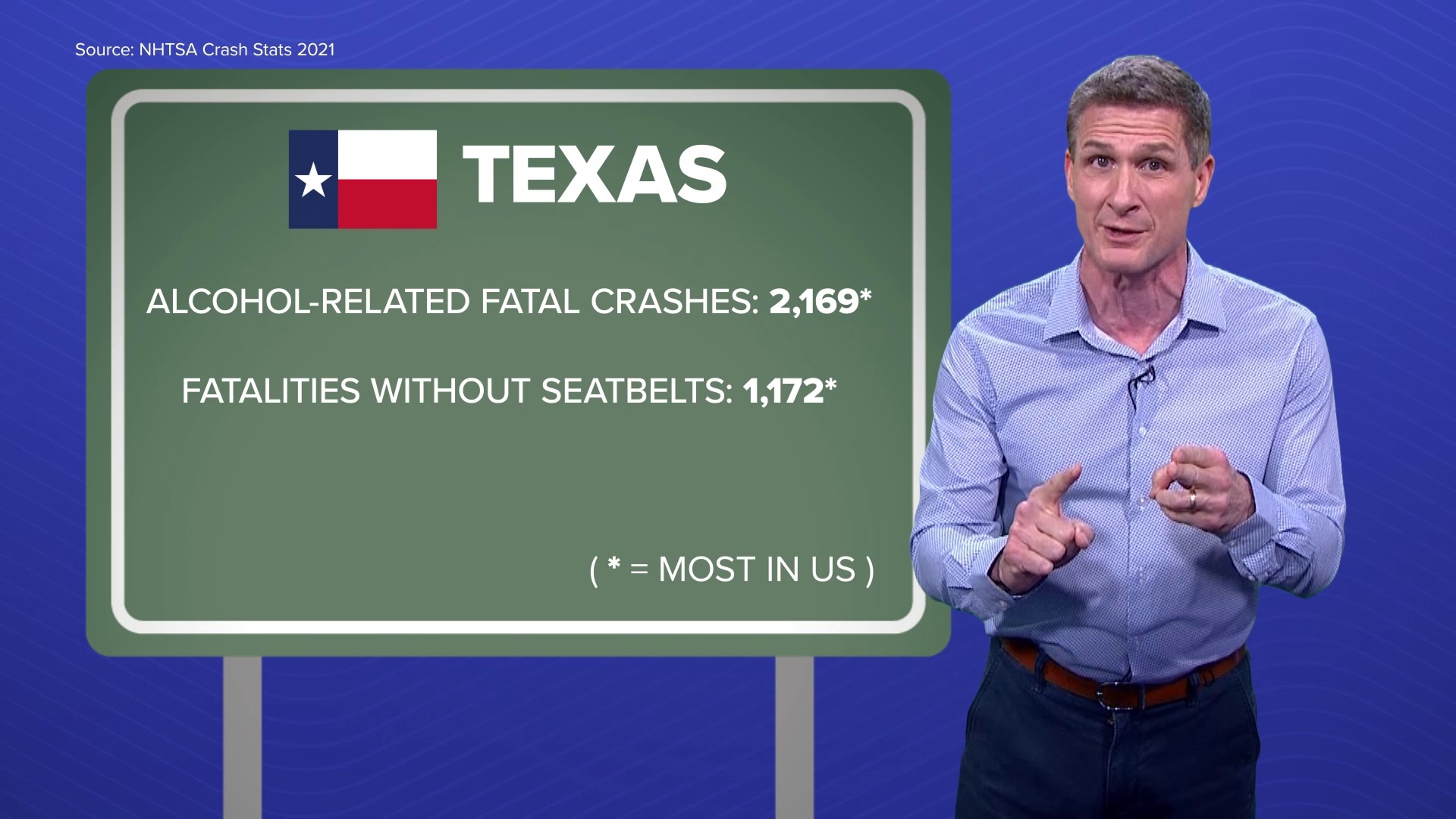

Yet, Texas had far more fatal crashes involving alcohol (2,169). Also, Texas had the most people not wearing seatbelts who died in crashes (1,172) . We also had more speeding-related fatalities (1,568). That’s just fatalities. In 2022, there were 162,414 speed-related crashes.

Texas isn’t No. 1 in auto thefts, but still has a lot of them

Now, according to the Insurance Information Institute, California once again stole the top spot for vehicle thefts last year, with 208,868 of them. Texas had 105,015 vehicle thefts, a distant second behind California.

Still, the total in the Lone Star State was almost as many thefts as the combined totals of the final four states in the top 10: Missouri (27,279 thefts), Georgia (28,171 thefts), Ohio (31,647 thefts) and New York (32,715 thefts).

Also, many autos on Texas roads are uninsured accidents waiting to happen. Last year the state counted 2,604,394 “unmatched registrations”. Many of those are suspected to be uninsured vehicles.

That might make you grip the steering wheel tighter. It also makes insurance premiums rise. Insurers hate that stat and all of the things listed above, because these problems increase the risk that they will have to pay out more in claims.

But insurers have plenty of money, right?

According to Texas Department of Insurance data, in 2020, auto insurers in Texas had combined auto policy profits of $2,894,463,942. But then they gave all that back and then some in 2021, 2022, and 2023, when they had huge losses year after year, totaling a combined - $3,753,242,443.

And that was even as they were raising premiums. That’s not a sustainable business model. So, buckle up. With numbers like those, it wouldn’t be surprising if we saw more increases ahead.

Lowering your auto insurance premium

It can help tremendously to shop around for insurance. Many times, a competitor may try to entice you and might offer a lower premium than your current one. So, I do that periodically. And you don’t have to wait for your current policy end-date to shop and switch.

It can also be beneficial to be married (but certainly don’t just do it for the insurance savings!) Oddly, that can help. Liberty Mutual says insurers see married people as “more stable and therefore, less of a risk”.

I realized some savings by increasing my collision and my comprehensive deductibles. Those are the amounts I have to pay if I file a claim. The lower the deductibles, the higher the premium, and vice versa. I didn’t like adjusting those, but it made a noticeable difference.

Also, like it or not, insurers are likely to consider your credit history when determining the risk of covering you.

And then there is usage based insurance

Usage based insurance is where the insurer gives you a device to put in your car and/or where you use your cell phone to monitor how much you drive, how often you brake hard, or speed.

I’m not ready to take that step yet. But admittedly, when I recently shopped around, those programs offered lower premiums. One insurer was willing to drop the premium by as much as 30% over time if I was considered a great driver.

Maybe that’s why this survey found last year that 17% of customers are giving it a whirl, more than double the number who signed up in 2016.