DALLAS — If your New Year's resolution is to save money, take a look at your calendar.

Rodney Anderson from Supreme Lending in Dallas says everyone should take a financial day off every month.

That doesn't mean you pick a day and spend with reckless abandon. Instead, a financial day off is a scheduled personal finance check-up.

Anderson recommends regularly reviewing your expenses to make sure you're not overspending.

In a conversation with WFAA, Anderson mentioned three expenses money-minded people should focus on:

- Interest rates

- Utility costs

- Insurance

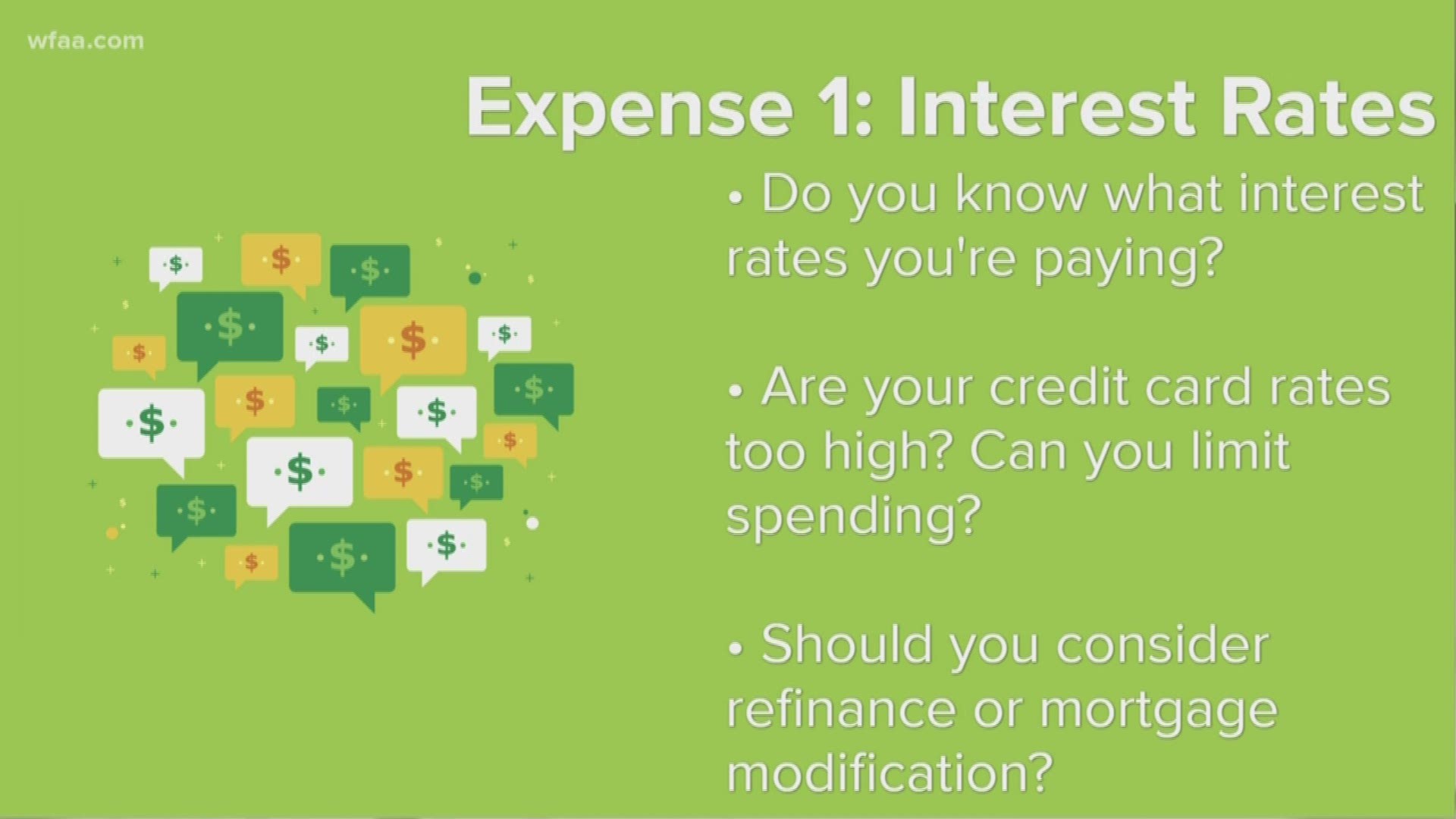

Interest Rates

When it comes to interest rates, Anderson mentioned three questions to consider.

- Do you know what interest rate you're paying?

- If your credit card interest rate is high, can you limit spending on that card to avoid high interest charges?

- If you're paying a high interest rate on your mortgage, is it worth exploring refinancing or a mortgage modification?

Utility Costs

Regularly reviewing your utility bills is another great way to search for savings, Anderson said.

Here are Anderson's three questions to ask to help find those savings.

- Do you know what your billable rate is for electricity, cable, cell phone, etc.?

- Have you shopped around to make sure your provider is giving you the best rate available?

- With cell phones and cable, have you reviewed your actual usage to make sure you're not overspending on the wrong plan?

Insurance

Not only should you shop around for the best rates on utilities, but Anderson said you should always shop around for better rates on home and auto insurance.

Anderson suggested asking your provider if there are discounts available for bundling home and auto insurance under one plan. In many cases, Anderson said, the discount is about 17%.

Not a Quick Fix

Financial security doesn't happen overnight, Anderson said. And, it doesn't happen if you only think about it on New Year's.

Anderson's advice, in addition to scheduling a financial day off, is to create a consistent review habit for all of your finances throughout the year.

If you save $50 a month, you may see that as a small saving. But over one year, that $50 turns into $600. Over five years, that turns into $3,000.

Think long-term.

And, of course, follow the basic wisdom of personal finance. Create and follow a budget. Pay off your debt. And keep track of your spending.

That's the sure-fire way to stick to your New Year's resolution.

RELATED: The best credit cards for families